In order to assess the immediate economic impacts of COVID-19 and understand the evolving business sentiment, we deployed a survey with our partners at San Diego Regional EDC, San Diego and Imperial Small Business Development Center. The Downtown San Diego Partnership and National City Chamber of Commerce also served as survey partners. The survey will remain open for the foreseeable future so we can chart how responses change over time.

Results from this survey will be published each Thursday and are available below. To receive these updates directly, sign up for our bi-weekly email updates.

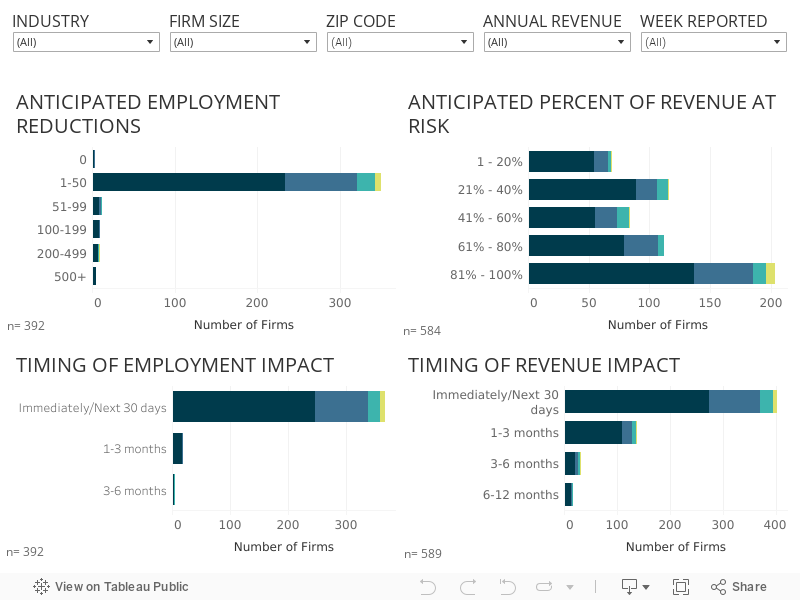

AN INTERACTIVE VISUALIZATION

Below is an interactive visualization of self-reported impacts to local employers, both in terms of employment and revenue. You can segment the data by industry, number of employees, and typical annual revenue.

RESPONDENT PROFILE

For up-to-date respondent information on the survey respondents and high level results, please view the responding profile here.

Results – April 16

Revenue impacts continue, but most firms favor temporary shutdowns over permanent closures

Three trends stood out based on what employers told us during the first four weeks of surveying. These findings are based on responses from 692 companies across the San Diego region:

- Few firms surveyed have closed permanently but temporary shutdowns are increasing. Only about 1% of survey respondents have permanently closed their business, but 42% have temporarily shut down operations. This is encouraging, since the number of local business closures could have a direct bearing on the pace of recovery once the COVID crisis subsides. Businesses that have permanently closed their doors are in a range of industries, including biotech and pharmaceuticals, cleantech, food and beverage, manufacturing, professional services, and retail.

- Vulnerable industries expect revenue impacts to continue. The industries in San Diego most vulnerable to the effects of policies aimed at containing the spread of the virus include arts and entertainment, food and beverage, retail, and tourism. Compared to when the survey began in mid-March, more firms in these industries increasingly expect revenue impacts to occur over the next 1-3 months, rather than immediately. The perception by business owners that the economic and financial pain of the crisis could last longer than initially expected will likely be reflected as an effective moratorium on business investment and hiring in the near term.

- More businesses seek financial assistance and access to capital. Compared to earlier survey results, more businesses are expressing interest in financing and capital to cope with the massive revenue shortfalls associated with COVID-19.

Results – April 9

Impacts are vast, amid signs of resiliency

Three trends stood out based on what employers told us during the first three weeks of surveying:

- Impacts are vast. 379 employers plan to eliminate 14,524 jobs; 68% of their combined workforce.

- Small businesses are embracing remote work. More than 85% of firms with remote workers are small businesses. Overall, 42% of employers surveyed are having employees work remotely.

- Some firms are still hiring. More than 11% of firms are still planning to fill positions. Nearly 19% of those firms still hiring are in the professional service industry.

Results – April 2

Immediate impacts are concentrated, severe, and hit small business & low wage workers hardest

More than 86% of businesses in San Diego expect to see revenue losses in the wake of COVID-19, according to an economic impact survey on the San Diego economy.

KEY TAKEAWAYS

Three trends stood out based on what employers told us during the first two weeks of surveying:

- Impacts are concentrated by industry. Of the 360 employers planning to reduce staff, 80% are in the food and beverage or tourism industries.

- Impacts are immediate. Nearly 94% of employers anticipating staffing reductions and two-thirds of those expecting revenue declines expect those hits within 30 days.

- Impacts disproportionately affect small businesses. Employers with annual revenues below $1M anticipate average losses in income of nearly 70%, compared with an average loss of 51% for businesses earning more than $1M annually.

A majority of employers (61%) are in need of capital support. More than half of those with capital needs are the smallest of employers with fewer than 5 employees.